The TAGMarkets System in the Shadow Realm of Mauritius: FMA Warning

As a financial and brokerage platform, TAGMarkets promotes itself online as a modern Forex, CFD, and cryptocurrency broker offering copy trading tools, high trading volumes, and numerous — sometimes exotic — account models. Yet behind the polished façade, significant warning signals, ambiguities, and substantial risks for investors become apparent, requiring a professional assessment.

Our analysis of internal documents and recent communications reveals the red flags of a system that appears to be under considerable pressure.

FMA-Warnung: TAGMarkets kein erlaubter Finanzdienstleister in Österreich

FMA Warning: TAGMarkets Not Authorized to Provide Financial Services in Austria

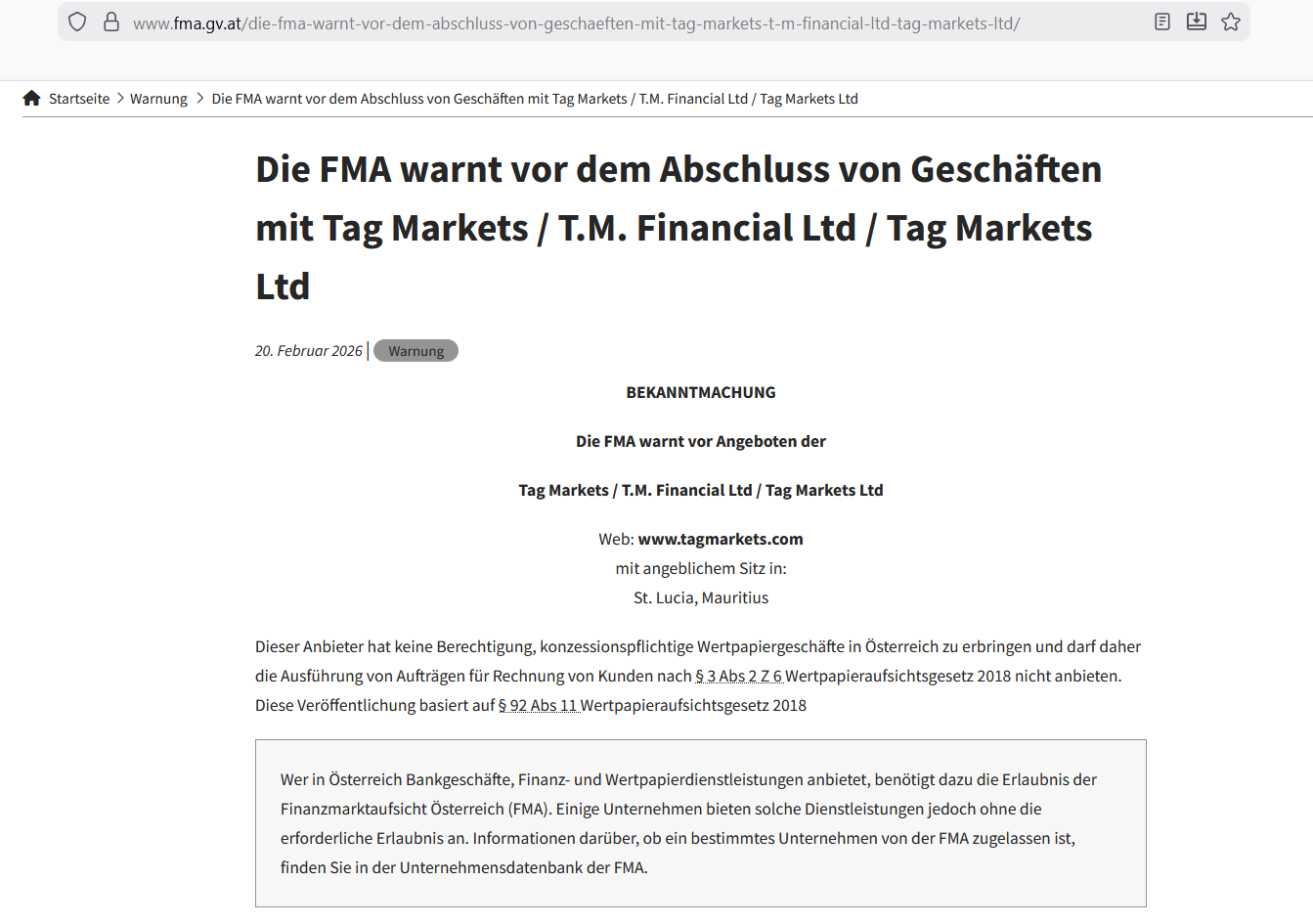

In several countries, regulatory warnings have already been issued against TAGMarkets, now including Austria. On February 20, 2026, the Austrian Financial Market Authority (FMA) published an official warning explicitly cautioning against entering into transactions with Tag Markets, T.M. Financials Ltd, and Tag Markets Ltd. In its formal notice, the authority stated that these providers are not authorized to conduct licensable securities transactions in Austria and therefore do not possess the legally required authorization to provide such services under the Austrian Securities Supervision Act 2018.

The FMA explains that companies offering banking, financial, or securities services in Austria are required to obtain a mandatory license, which can be verified in the authority’s official company database. As Tag Markets is not listed among the approved financial service providers, the company is not permitted under Austrian law to execute such transactions for clients.

This warning is significant because it represents not merely a regulatory notice but also signals a legal risk for investors. Any entity offering financial services in Austria or the European Union without the appropriate authorization is in breach of supervisory law — and investors are consequently far less protected. As FMA warnings are typically issued when a provider offers or performs unauthorized financial services, the notice underscores that Tag Markets is not permitted to operate as a licensed broker within the EU legal framework.

For potential investors, this is more than a bureaucratic label. Without official authorization, access to established consumer protection mechanisms, complaint procedures, and legal enforceability at the national level is effectively eliminated — safeguards that are considered standard in regulated markets such as Germany or Austria.

Glänzende Oberfläche, regulatorischer Graubereich

Polished Surface, Regulatory Grey Area

At first glance, TAGMarkets appears to be a modern, internationally positioned online broker. The website is professionally designed, promoting transparency, technological innovation, and the use of the established trading platform MetaTrader 5 (MT5). For many retail investors, this is a familiar signal: MT5 is globally recognized as standardized trading infrastructure in the Forex and CFD sector.

However, technology alone is not a quality indicator. What matters is the regulatory framework — and this is precisely where the tension begins.

Officially, the platform is operated by T.M. Financials Ltd. The company is registered in Mauritius and holds a license from the local Financial Services Commission. Formally, it is therefore a regulated provider. Substantively, however, the difference lies in the details: regulatory oversight in Mauritius is not comparable to the stringent requirements of European financial market regulation. We previously reported on this offshore license as a fig leaf in connection with the sales activities of former Lyoness/Lyconet/Safir/ZENIQ marketer Werner Kaiser.

While institutions within the EU operate under the MiFID II regime and are supervised by authorities such as Germany’s Federal Financial Supervisory Authority (BaFin) or the Austrian Financial Market Authority (FMA), offshore licenses do not offer comparable deposit protection, transparency obligations, or capital requirements. For investors, this means that in the event of a dispute, the familiar European protection mechanisms do not apply.

The hardware in question likely exists only on paper (“phantom hardware”) in order to circumvent the classification of a prohibited financial product. The suspected objective: by declaring the product as a “hardware sale,” the operators attempt to avoid strict EU regulations such as MiCA or oversight by the U.S. Securities and Exchange Commission (SEC). Disclaimers explicitly state that there are “no guarantees of returns or capital repayment.” For investors, this effectively means a complete loss of statutory investor protection.

Mauritius: The Offshore-Construct

For years, Mauritius has been a popular jurisdiction for financial service providers operating internationally while seeking to avoid the full weight of European regulatory pressure. Registration alone therefore says little about the actual economic substance of a company.

Additionally, many offshore brokers operate using so-called white-label solutions. The technical infrastructure — trading servers, price feeds, and settlement systems — is provided by specialized third parties. The brand name under which investors trade is often interchangeable. This makes it difficult to determine who ultimately benefits economically and who bears operational responsibility.

In the grey market, a recurring pattern can be observed: when a brand becomes burdened by negative reporting, a similarly structured offering often reappears shortly thereafter under a new name.

In the case of TAGMarkets, matters are aggravated by the misuse of a defunct license, as we previously reported in our article on regulation as façade.

Despite clear confirmation, the non-existent license continues to be promoted by T.M. Financials Ltd and Tag Markets as a mark of quality. These companies present themselves as “regulated brokers,” although verification shows that neither a current supervisory status exists nor any historical connection between the license and T.M. Financials ever existed. This constitutes a case of regulatory misrepresentation that systematically undermines the risk awareness of inexperienced or previously harmed investors.

The license in question (GB21026474) was held by Pure North Markets Ltd, surrendered on March 27, 2024, and has not been reissued since.

The Role of NEO.FX and EXFusion in the Sales Structure

A central component of the current structure is the linkage between TAGMarkets and the brands NEO.FX and EXFusion. While TAGMarkets acts as the broker infrastructure and provides the actual trading accounts via the MetaTrader 5 platform, NEO.FX and EXFusion clearly function as upstream sales and product labels.

NEO.FX is presented in webinars and promotional materials as an automated trading strategy or copy trading solution activated through an account held with TAGMarkets. No independent financial services license is apparent in this context; operational execution occurs exclusively through the broker structure of T.M. Financials Ltd.

EXFusion, in turn, presents itself as a network or affiliate project attracting participants through referral marketing, training programs, and community-based models. Registration within this structure effectively leads to the opening of a trading account with TAGMarkets, through which strategies such as NEO.FX are then to be used. This creates a division of roles: TAGMarkets provides the technical and formal brokerage shell, while EXFusion organizes distribution and NEO.FX serves as the marketed trading solution. For investors, this separation is not always transparent. Economically, however, deposits and trading activities ultimately flow to the offshore entity, while marketing, training, and recruitment take place outside the actual broker structure.

TAGMarkets Sales Actors with a History: Werner Kaiser, Asker Sakinmaz

Within the TAGMarkets environment, sales actors appear who were previously active in earlier, sometimes heavily criticized business models. Among them is Werner Kaiser, known in German-speaking countries as a leading distributor within the Lyconet/Lyoness network. These structures were for years the subject of scrutiny by consumer protection groups, media, and courts, as they were accused of operating a heavily commission-driven system with pyramid-like elements. In later phases, Kaiser also appeared in connection with dubious crypto and token projects such as Safir/ZENIQ, XERA, and XPRO.

Another name is Asker Sakinmaz, who likewise originates from the network marketing sector and has been active over the past decade in various international sales structures involving at least questionable financial and crypto products such as Safir/ZENIQ. Observers classify him among those actors who scale new investment offerings primarily through referral marketing and webinar-based structures.

Prior involvement in controversial business models does not in itself constitute proof of current misconduct. From an investigative perspective, however, the continuity of personnel is noteworthy. When the same sales actors who previously promoted commission-driven network models now advocate offshore brokers and automated trading solutions, legitimate questions arise regarding business logic, sustainability, and the protection of investor interests.

The Legal Dilemma for Investors

Ultimately, the greatest risk lies less in the trading product itself than in the enforceability of claims. In the event of disputes, European clients would need to assert their claims against a company based in Mauritius. This entails high costs, complex questions of international jurisdiction, and uncertain prospects of enforcement.

TAGMarkets is therefore an offshore broker operating under a regulatory framework that does not correspond to European standards. Combined with aggressive online marketing, structural opacity, and documented withdrawal complaints, the resulting risk profile significantly exceeds that of an EU-regulated institution.

For investors, this requires a sober assessment: anyone engaging with such a construct deliberately leaves the protective sphere of European financial supervision and enters an environment where legal enforcement options are limited. In a market built on trust, that is the decisive factor.

Note:

This article is a journalistic analysis. It is based on publicly available sources. It is not a legal assessment or financial advice. All assessments have been researched to the best of our knowledge and are marked as opinions within the meaning of Art. 10 ECHR / Art. 5 GG. Counterstatements will be taken into account in accordance with § 56 RStV.

Sources:

- FMA.gv.at

- TAGMarkets, XFusion & NeoFx Telegram Groups

- Own Verification (Editorial Team)

Leave a Reply

Want to join the discussion?Feel free to contribute!